Contact Sales

Year after year, we hear the same warning: millions of Americans are just one unexpected expense away from a crisis. Financial stress is taking a significant toll on today’s workforce – showing up as reduced productivity, increased turnover, and delayed retirement. The good news? There’s a clear solution.

Our latest survey highlights the growing impact of emergency savings programs and how they can improve financial well-being, support retention, and strengthen workforce resilience. As Stephen Roll, Research Director at Washington University, puts it: “Emergency savings is one of the single best predictors of a person’s financial well-being.”

This blog summarizes the key findings from our research and explores how emergency savings programs offer an effective path forward for employers who want to support their workforce and strengthen long-term business outcomes.

Financial stress is the new normal

Financial stress is no longer the exception – it’s the reality for most American workers. Our research found that 71% of Americans experience moderate-to-extreme financial stress, with consistent findings across regions. The numbers climb higher still for women (77%) and those earning less than $50,000 a year. Meanwhile, nearly half of all workers (49%) report having less than one month’s worth of emergency savings.

But behind these statistics are real people. One respondent shared that she had to take paid time off to work a second job just to cover an unexpected cost. Another described how the burden of juggling property and income tax demands with urgent home repairs had led him to sell investments. One participant explained that when his car broke down, he didn’t have the funds for repairs and was unable to rely on others or afford Uber.

These personal stories reflect the deeper challenges facing growing numbers of American workers. Financial instability is widespread, and the issues are varied and urgent.

Productivity: Financial stress reduces performance at work

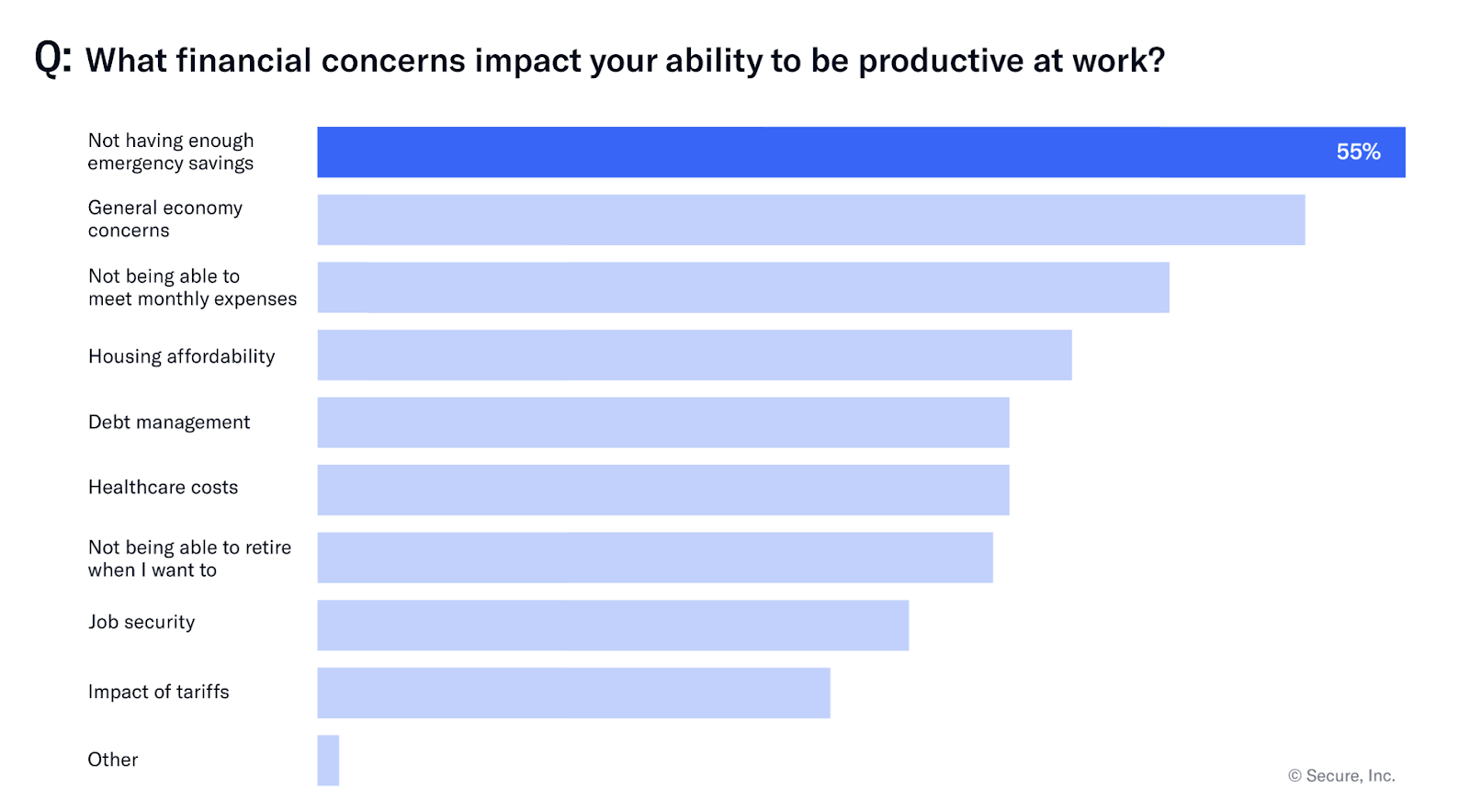

Without meaningful support, even a single unexpected expense can throw a household into crisis – and the ripples extend into the workplace. A striking 55% of survey respondents said that not having enough emergency savings negatively affected their ability to remain productive at work. In fact, it topped the list of productivity disruptors, outranking concerns about the broader economy, monthly expenses, housing costs, debt, and even healthcare.

The consequences are tangible: nearly 40% of employees reported missing work in the past six months due to financial stress. That’s time lost for individuals and productivity lost for employers.

However, the research also uncovered a clear solution. Employees with more than two months’ worth of emergency savings reported significantly better performance and fewer days missed. Those with six or more months of emergency savings had the lowest rates of absenteeism – a clear demonstration of how a financial cushion can dramatically improve focus, attendance, and well-being at work.

Emergency savings: An untapped driver of employee retention

With 44% of employees actively looking for a new job, retention is already a significant challenge for employers. At the same time, data from our survey reveals just how closely emergency savings and job stability are linked.

Workers with less than three months of savings are 76% more likely to be job hunting compared to those with a stronger financial buffer. In contrast, only 1 in 5 employees with at least six months of emergency savings are actively seeking a new role.

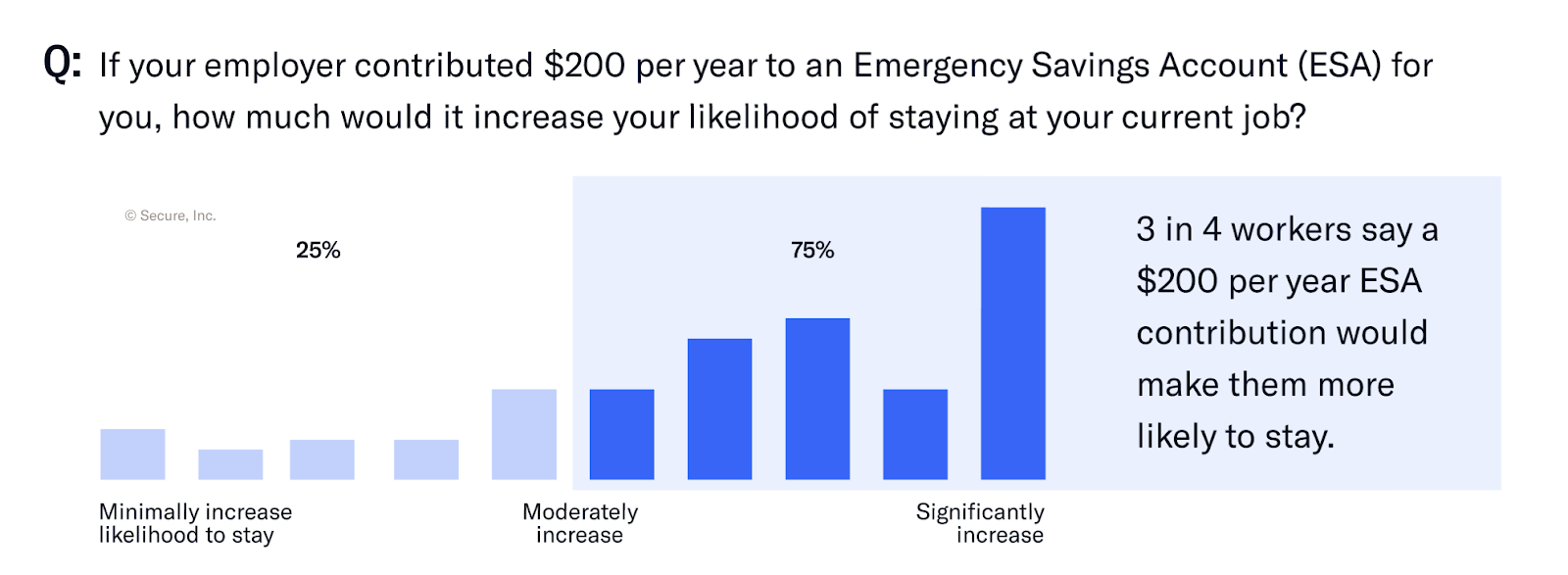

We asked respondents how an employer-sponsored emergency savings program might influence their decision to stay. The response was clear: 3 in 4 workers said that even a modest contribution – $200 per year – to an Emergency Savings Account (ESA) would increase their likelihood of remaining with their current employer.

Retirement readiness: Short-term financial woes impact long-term stability

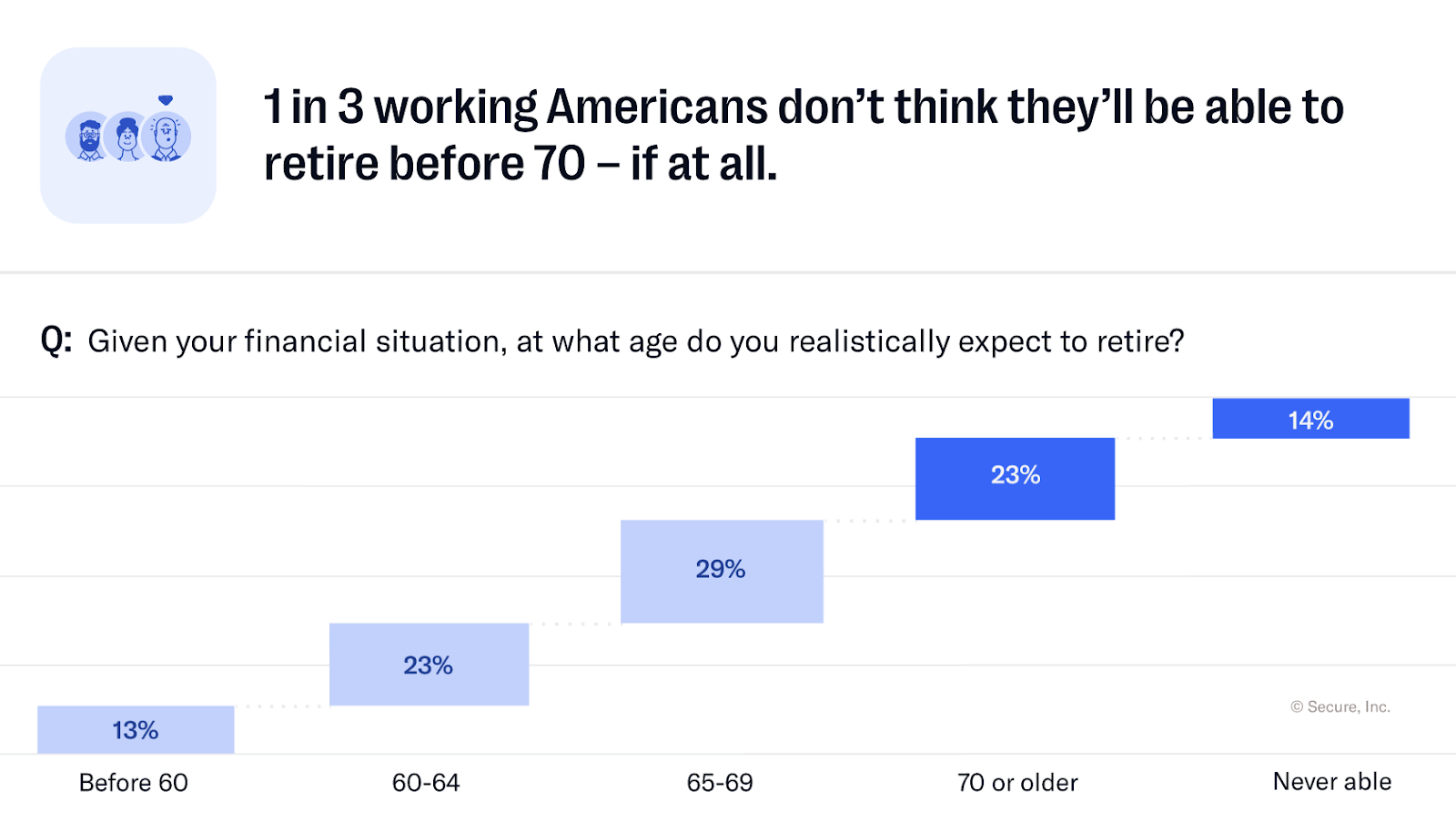

For many Americans, the dream of retiring on time is slipping further out of reach. One in three don’t believe they’ll be able to retire before age 70 – if at all.

However, the connection between emergency savings and long-term financial stability is undeniable. Without a financial cushion, workers are far more likely to pause or reduce their retirement contributions to manage unexpected costs.

The survey shows that this pattern changes significantly when emergency savings are in place. Among those with at least six months’ worth of savings, only 10% reported adjusting their retirement plans in response to financial hardship, compared to 48% of those with little or no savings.

Emergency savings programs: A clear path forward

Ultimately, short-term financial stress is a workplace issue with measurable business consequences, including reduced productivity, higher turnover, and delayed retirement. But employers have the power to take action. Workplace emergency savings programs offer a practical, proven solution that supports employee well-being and strengthens organizational performance.

Our purpose-built ESA is designed to drive real impact, with over 60% employee participation, an intuitive digital experience, automated payroll contributions, and flexible employer incentives. It’s the first financial wellness benefit proven to sustain long-term saving behavior, at scale.

Read the full findings to explore how emergency savings can help your workforce and your business thrive. Or get in touch for more information on workplace emergency savings.